The Roth IRA is widely considered the most valuable retirement account available to individual savers. Tax-free growth, tax-free withdrawals, no required minimum distributions during your lifetime, flexible access to contributions, and strong estate planning advantages. It is also the account the IRS restricts based on income — which means the people who need tax diversification most are exactly the ones who cannot access it directly.

The backdoor Roth IRA is a fully legal two-step workaround that eliminates the income limit. It requires no special account type and no IRS approval. It takes advantage of rules that have existed in the tax code for over a decade and has been explicitly acknowledged in congressional proceedings.

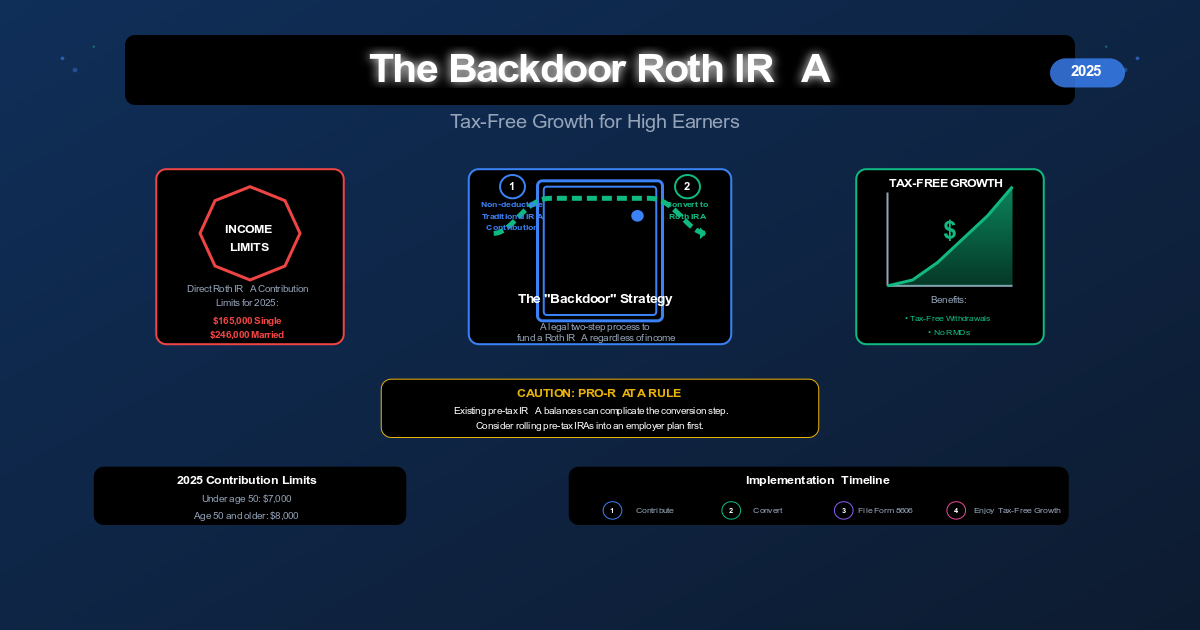

The Income Limit Problem

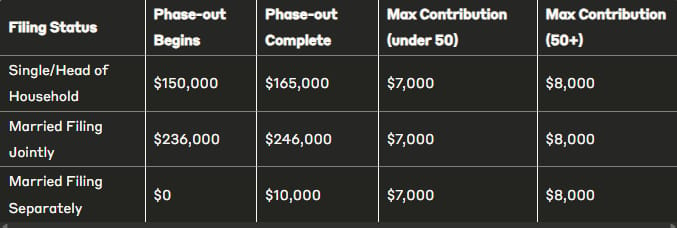

Direct Roth IRA contributions phase out and eventually become unavailable above certain MAGI thresholds:

| Filing Status | Phase-Out Begins | Fully Phased Out | Direct Roth Allowed? |

|---|---|---|---|

| Single / Head of Household | $150,000 | $165,000 | No above $165,000 |

| Married Filing Jointly | $236,000 | $246,000 | No above $246,000 |

| Married Filing Separately | $0 | $10,000 | No above $10,000 (if lived with spouse) |

Real examples:

- Jennifer, a 42-year-old physician earning $280,000 — cannot contribute directly

- Mark and Sarah, combined income $300,000 — cannot contribute directly

The backdoor Roth converts this hard stop into a detour.

How the Backdoor Roth Works: 2 Steps

| Step | Action | Why It Works |

|---|---|---|

| Step 1 | Make a non-deductible contribution to a Traditional IRA | No income limit applies to IRA contributions — only to deductibility |

| Step 2 | Convert the Traditional IRA to a Roth IRA | Conversions have no income limit (this rule has applied since 2010) |

The tax mechanic that makes this work: non-deductible contributions go in with after-tax dollars. When you convert after-tax dollars to a Roth IRA, there is nothing to tax — the money was never deducted. If you convert before any earnings accumulate, the tax bill is zero or minimal.

Step-by-Step Implementation

Step 1: Open a Traditional IRA (If Needed)

Open a Traditional IRA at any major custodian — Fidelity, Schwab, and Vanguard all offer no-fee Traditional IRAs. If you already have existing Traditional IRA balances, read the pro-rata section below before proceeding.

Step 2: Make a Non-Deductible Contribution

| Detail | Amount |

|---|---|

| Contribution limit (under 50) | $7,000 |

| Contribution limit (age 50+) | $8,000 |

| Earned income requirement | Must have earned income at least equal to the contribution |

| Deadline for prior-year contributions | April 15 of the following year |

Critical: Do not check the box indicating the contribution is deductible. High earners with workplace retirement plans are not eligible to deduct Traditional IRA contributions anyway, but explicitly making a non-deductible contribution establishes the basis that prevents future double taxation.

File Form 8606 with your tax return every year you make a non-deductible contribution. This form creates the official IRS record of your after-tax basis. Without it, the IRS has no record that you already paid tax on this money, and you could be taxed again when you convert or withdraw.

Step 3: Convert to a Roth IRA

Log into your brokerage account and initiate a Roth conversion of the Traditional IRA balance. Most custodians call this a “Roth conversion” or “Roth rollover” in their online interface.

Timing: No mandatory waiting period exists between contribution and conversion. Convert as soon as the contribution settles — typically 1 to 3 business days. The goal is to minimize earnings that accumulate in the Traditional IRA before conversion, because those earnings become taxable.

Some advisors suggest waiting 30 to 60 days to reduce any appearance of a pre-planned “step transaction” — discussed further below. This is a judgment call; the IRS has not challenged the strategy for prompt conversions.

Step 4: Report on Your Tax Return

File Form 8606 again in the year of conversion to report:

- The non-deductible contribution (Part I)

- The Roth conversion amount (Part II)

- The taxable portion (should be $0 or minimal if converted promptly)

You will receive a Form 1099-R from your custodian for the conversion. The taxable amount shown may appear incorrect — Form 8606 is what reconciles this by establishing your basis.

The Pro-Rata Rule: The Most Important Consideration

The pro-rata rule is where most backdoor Roth mistakes happen. Understanding it before you start prevents an unexpected tax bill.

What the Pro-Rata Rule Does

The IRS does not allow you to select which dollars you convert. Every conversion is treated as a proportional mix of all your Traditional, SEP, and SIMPLE IRA balances — pre-tax and after-tax combined.

Formula:

Taxable % of conversion = Pre-tax IRA balance / Total IRA balance (all accounts)The Pro-Rata Problem in Action

Michael’s situation:

| Item | Amount |

|---|---|

| Existing rollover IRA (pre-tax, from old 401k) | $93,000 |

| New non-deductible contribution | $7,000 |

| Total IRA balance | $100,000 |

Michael converts $7,000 to Roth. Pro-rata calculation:

| Component | Calculation | Amount |

|---|---|---|

| After-tax percentage | $7,000 / $100,000 | 7% |

| Pre-tax percentage | $93,000 / $100,000 | 93% |

| Tax-free portion of conversion | 7% x $7,000 | $490 |

| Taxable portion of conversion | 93% x $7,000 | $6,510 |

| Tax owed at 32% bracket | $6,510 x 32% | $2,083 |

Michael’s $7,000 backdoor Roth contribution triggers a $2,083 tax bill — not because of the strategy itself, but because of the existing pre-tax IRA balance.

How to Eliminate the Pro-Rata Problem

| Solution | How It Works | Timing |

|---|---|---|

| Roll pre-tax IRA into employer 401(k) | Most 401(k) plans accept IRA rollovers; removes the pre-tax balance from the pro-rata calculation | Must be completed by December 31 of the conversion year |

| Convert all Traditional IRA assets | If you convert everything, pro-rata applies but you address all balances at once — no pre-tax remainder | Requires paying full tax on the pre-tax portion |

| Never accumulate pre-tax IRA balances | Structure rollovers from prior employers directly into the new 401(k) rather than into an IRA | Proactive — prevent the problem rather than solve it |

Michael’s smart fix: Before implementing the backdoor Roth, Michael rolls his $93,000 rollover IRA into his current employer’s 401(k). His only IRA balance is now the $7,000 non-deductible contribution. When he converts, the taxable amount is $0.

Which IRA balances trigger pro-rata:

| Counts Toward Pro-Rata | Does NOT Count |

|---|---|

| Traditional IRAs | Roth IRAs |

| Rollover IRAs | 401(k), 403(b), 457(b) |

| SEP IRAs | |

| SIMPLE IRAs (after 2-year seasoning) |

The pro-rata calculation uses your December 31 balance for the year of conversion — not the balance at the time of the conversion itself. Roll pre-tax IRAs into a 401(k) before year-end to clear them from the calculation.

Benefits Worth Repeating

| Benefit | Why It Matters for High Earners |

|---|---|

| Tax-free growth | Decades of compounding without annual capital gains or dividend taxes |

| Tax-free withdrawals | Qualified distributions not counted as income — no impact on Medicare IRMAA, Social Security taxation, or future bracket management |

| No RMDs | Unlike Traditional IRAs, Roth IRAs have no required minimum distributions during the owner’s lifetime |

| Tax diversification | Combination of pre-tax and Roth accounts gives retirement income flexibility to manage tax brackets year by year |

| Estate planning | Beneficiaries inherit Roth IRAs and take distributions tax-free (subject to 10-year distribution rules under SECURE Act) |

| Hedge against rate increases | Conversions lock in today’s tax rate on today’s dollars; future withdrawals are tax-free regardless of future rates |

The compounding math: $7,000 contributed annually for 25 years at 7% annual return = approximately $438,000. In a Roth IRA, every dollar of that $438,000 is tax-free in retirement. In a taxable account, gains are taxed annually and the balance on withdrawal is subject to capital gains tax.

4 Common Mistakes

Mistake 1: Not filing Form 8606

Without Form 8606, the IRS has no record of your after-tax basis. You will be taxed again on money you already paid tax on when you withdraw or convert. File it every year you make a non-deductible contribution — and keep copies indefinitely.

Mistake 2: Ignoring existing Traditional IRA balances

Assuming the conversion is tax-free without checking whether the pro-rata rule applies. Calculate the tax consequence before contributing. If pro-rata is a problem, solve it first by rolling pre-tax IRAs into a 401(k).

Mistake 3: Letting earnings accumulate before conversion

Waiting weeks or months after contribution allows earnings to accumulate. Those earnings are taxable at conversion. Convert within days of the contribution settling.

Mistake 4: Thinking this strategy bypasses annual limits

The $7,000 / $8,000 annual contribution limit still applies. The backdoor Roth removes the income restriction — it does not increase the contribution cap.

The Step Transaction Concern

Some tax professionals raise the “step transaction doctrine” — a principle that allows the IRS to recharacterize a series of related steps as a single transaction. In theory, the IRS could view contribution + immediate conversion as a single direct Roth contribution, violating the income limits.

In practice, this concern has diminished substantially:

- The strategy has been openly discussed in congressional hearings

- Proposed 2021 legislation would have explicitly eliminated the strategy — which implicitly acknowledged it is currently legal

- The IRS has had over a decade to challenge the practice and has not done so

- The IRS itself provides instructions for Form 8606 that contemplate this exact scenario

A 30 to 60-day gap between contribution and conversion reduces any theoretical risk further, though there is no requirement to wait.

Implementation Timeline for the Current Tax Year

| Window | Action |

|---|---|

| January — December (current year) | Verify you will exceed income limits; check for existing IRA balances that trigger pro-rata; roll pre-tax IRAs into 401(k) before December 31 if needed |

| As early as January | Make non-deductible Traditional IRA contribution for the current year; convert to Roth shortly after settlement |

| January — April 15 (following year) | Can still make prior-year contribution up to the tax filing deadline; convert promptly after contribution |

| Tax filing | File Form 8606 reporting the non-deductible contribution and the conversion; reconcile with Form 1099-R from custodian |

Front-loading the contribution early in the year maximizes the time the Roth account has to grow tax-free.

Is the Backdoor Roth Right for You?

| Situation | Fit |

|---|---|

| Income exceeds direct Roth IRA contribution limits | Required — this is the core use case |

| No existing pre-tax IRA balances (or can roll them into a 401k) | Strong fit |

| Other tax-advantaged accounts (401k, HSA) already maximized | Strong fit — this is the natural next step |

| Expect same or higher tax bracket in retirement | Strong fit — paying tax now is advantageous |

| Significant pre-tax IRA balances with no 401k to absorb them | Evaluate carefully — pro-rata may make this inefficient |

| Expect significantly lower tax bracket in retirement | Traditional contributions may be more efficient |

| Other tax-advantaged accounts not yet maximized | Address those first — 401(k) match, HSA, then backdoor Roth |

This article is for educational and informational purposes only and should not be construed as personalized tax, financial, or legal advice. Tax laws are complex and subject to change. Contribution limits, income thresholds, and form requirements referenced here are based on current law and are subject to adjustment by the IRS or Congress. Individual circumstances vary significantly — consult a qualified tax professional, CPA, enrolled agent, or financial advisor before implementing any strategy discussed here.