Your business just had its best year ever. You diligently paid every dollar of tax you owed by April 15th. Three weeks later, the IRS sends you a penalty notice for thousands of dollars.

Sound familiar? Here is why this happens — and how to prevent it permanently.

The Penalty Trap That Catches Good Taxpayers

The IRS operates on a “pay-as-you-go” system designed for traditional employees with steady paychecks. For a salaried employee, taxes are withheld evenly across every paycheck throughout the year. For a business owner, freelancer, or investor with irregular income, the expectation is 4 equal estimated payments — even if most of your income arrives in Q4.

The cruel irony: Even if you pay your entire tax bill by April 15th, the IRS can still assess penalties for not paying “on time” throughout the prior year. Paying in full at filing is not the same as paying evenly throughout the year.

The Safe Harbor Rule: Your Penalty Shield

Think of Safe Harbor as insurance against underpayment penalties. Follow the rules, and the IRS cannot assess penalties — period.

The key insight: Safe Harbor does not require you to predict the future. Instead, it uses your known prior-year results to create a predictable payment schedule for this year.

The 3 Safe Harbor Options

| Option | Requirement | Best For |

|---|---|---|

| Option 1: 90% of current year | Pay 90% of this year’s actual tax liability | When income is declining or predictable |

| Option 2: 100% of prior year | Pay 100% of last year’s total tax (Line 24) | AGI of $150,000 or less |

| Option 3: 110% of prior year | Pay 110% of last year’s total tax (Line 24) | AGI over $150,000 — the most reliable option for high earners |

For most entrepreneurs and high earners, Option 3 is the right choice. It eliminates guesswork entirely and protects against any income level — even a year where revenue doubles or triples.

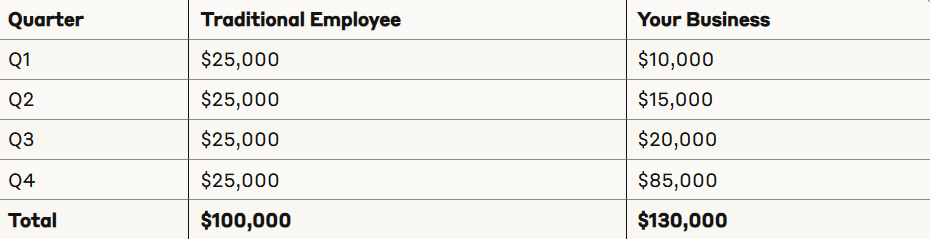

How Safe Harbor Works: A Real Example

Maria’s situation:

| Item | Amount |

|---|---|

| Last year’s federal tax (Form 1040, Line 24) | $42,000 |

| Last year’s AGI | $220,000 (above the $150K threshold) |

| This year’s business | Exploding — actual tax will be $75,000 |

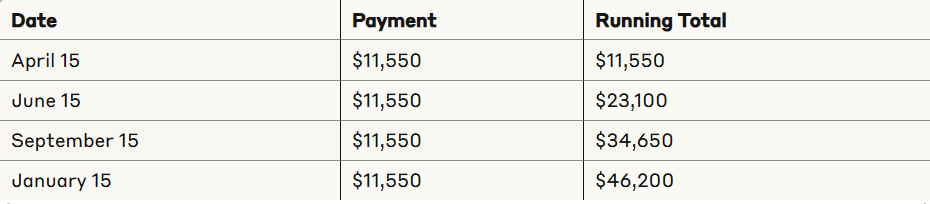

Maria’s Safe Harbor calculation:

Safe Harbor Target = $42,000 × 110% = $46,200

Quarterly Payment = $46,200 ÷ 4 = $11,550Maria’s payment schedule:

| Deadline | Payment | Cumulative |

|---|---|---|

| April 15 (Q1) | $11,550 | $11,550 |

| June 15 (Q2) | $11,550 | $23,100 |

| September 15 (Q3) | $11,550 | $34,650 |

| January 15 (Q4) | $11,550 | $46,200 |

The result: Maria’s actual tax liability jumps to $75,000 — $28,800 more than her Safe Harbor target.

| Approach | Outcome |

|---|---|

| Traditional (no Safe Harbor) | Penalties on the $21,750 quarterly shortfall |

| Safe Harbor | $0 penalties, despite being $28,800 “short” |

Maria pays the $28,800 balance when she files — but pays zero in penalty dollars. Safe Harbor bought her complete protection regardless of how dramatically her income grew.

Why Safe Harbor Works for Growing Businesses

Predictability over guesswork. Traditional estimated tax planning asks “What will I earn this year?” — an impossible question for most business owners. Safe Harbor asks “What did I earn last year?” — a question with a definitive answer on your prior return.

Cash flow management. Consistent, predictable quarterly payments let you plan cash reserves in advance. No scrambling at quarter-end to estimate a moving target.

Growth protection. Income can double, triple, or 10x. Your penalty exposure stays at zero as long as you hit your Safe Harbor target.

Your Safe Harbor Implementation Toolkit

Step 1: Find Your Numbers

Pull last year’s Form 1040 and locate 2 critical lines:

| Line | What It Is | Why It Matters |

|---|---|---|

| Line 11 | Adjusted Gross Income (AGI) | Determines which Safe Harbor percentage applies (100% vs. 110%) |

| Line 24 | Total Tax | The base for your entire Safe Harbor calculation |

Step 2: Calculate Your Safe Harbor Target

AGI of $150,000 or less: Safe Harbor Target = Line 24 × 100%

AGI over $150,000: Safe Harbor Target = Line 24 × 110%

Step 3: Set Your Quarterly Payment

Quarterly Payment = Safe Harbor Target ÷ 4

Step 4: Mark Your Calendar

| Quarter | Deadline | Covers Income Received |

|---|---|---|

| Q1 | April 15 | January through March |

| Q2 | June 15 | April through May |

| Q3 | September 15 | June through August |

| Q4 | January 15 | September through December |

Critical: Missing any deadline by even 1 day voids Safe Harbor protection for that quarter. Treat these dates as non-negotiable.

Interactive Calculation: Your Safe Harbor Number

Work through this with your prior-year return in hand:

| Step | Your Numbers |

|---|---|

| Line 24 (Total Tax) | $ _______ |

| Line 11 (AGI) | $ _______ |

| Safe Harbor % (100% if AGI ≤ $150K; 110% if AGI > $150K) | _______ % |

| Safe Harbor Target (Line 24 × %) | $ _______ |

| Quarterly Payment (Target ÷ 4) | $ _______ |

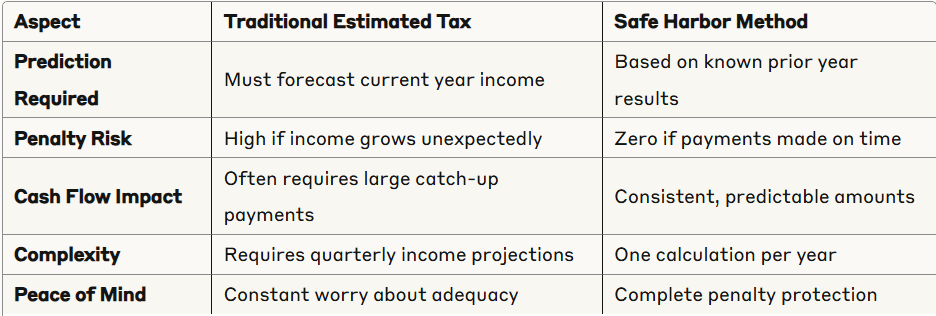

Safe Harbor vs. Traditional Planning: Side by Side

| Factor | Traditional Approach | Safe Harbor |

|---|---|---|

| Basis for payments | Estimated current-year income | Verified prior-year tax return |

| Penalty risk | High — any estimation error triggers penalties | Zero — as long as payments are timely |

| Calculation complexity | Requires forecasting income every quarter | One calculation per year |

| Growth scenario | Penalties increase as business grows | No penalties regardless of income growth |

| Cash flow planning | Unpredictable, varies by quarter | Consistent, predictable quarterly amounts |

4 Common Mistakes That Kill Safe Harbor Protection

Mistake 1: Using the wrong tax number

Wrong: Using your AGI, total tax including self-employment tax, or tax before credits. Right: Use Line 24 from Form 1040 — your actual income tax liability after all credits.

Mistake 2: Missing deadlines

Safe Harbor protection disappears entirely if any quarterly payment is late. Even 1 day late eliminates protection for that quarter. Late payment still reduces total penalties, but the Safe Harbor shield is gone.

Mistake 3: Forgetting state taxes

Safe Harbor only protects federal underpayment penalties. Every state has its own rules. Research your state’s requirements separately — some states offer no Safe Harbor protection at all.

Mistake 4: Assuming Safe Harbor covers everything

Safe Harbor prevents penalties — not additional taxes. If you owe a balance beyond your Safe Harbor payments, you pay it at filing. The difference is you pay it penalty-free.

3 Advanced Safe Harbor Strategies

The Conservative Cushion Approach

Pay 105% of your Safe Harbor requirement as a buffer against calculation errors and to reduce the balance owed at filing:

Enhanced Target = Safe Harbor Target × 105%A small premium for significantly more peace of mind — especially useful in years where income is expected to grow materially.

The Cash Flow Optimization Method

If your business receives predictable payments at the start of each quarter but faces heavy expenses near quarter-end, make estimated payments early in the quarter rather than scrambling at the deadline.

Example — Mark’s marketing agency:

| Item | Details |

|---|---|

| Q2 payment due | June 15 ($8,000) |

| Cash pattern | June 1 to 5: $25,000 in client retainers arrive |

| June 10 to 15 | $18,000 in project expenses and payroll |

Mark’s strategy: He pays his Q2 estimated tax on June 2nd when cash is flush — not June 15th when it’s tight. If an unexpected expense hits mid-June, his tax payment is already handled.

The Multi-State Coordination Strategy

Operating in multiple states creates overlapping obligations that don’t coordinate with each other. Each state has its own Safe Harbor rules, deadlines, and income allocation methods.

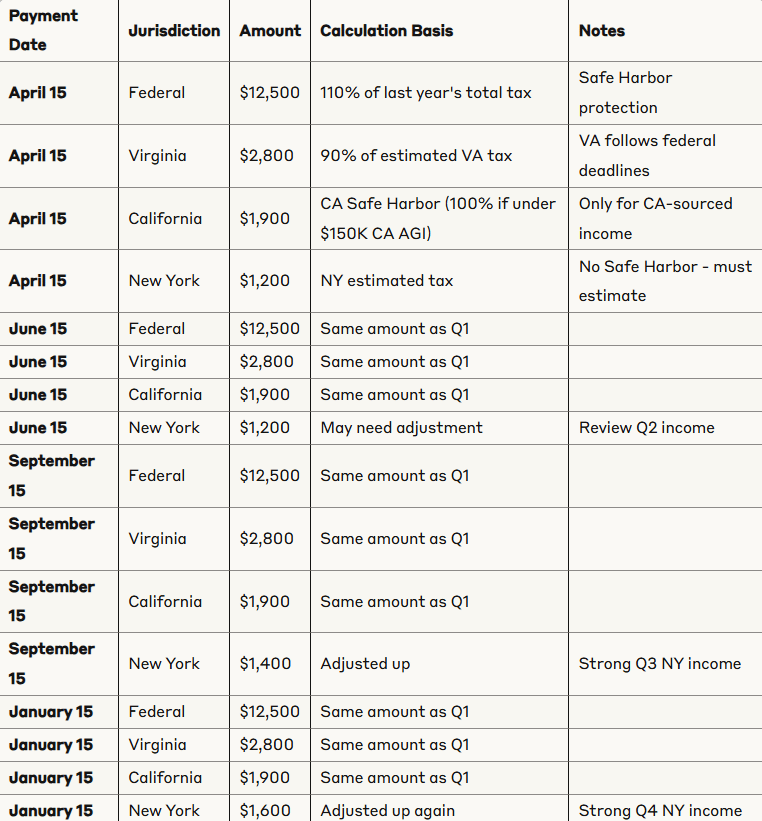

Example — Jennifer’s situation: She lives in Virginia, consults for clients in California and New York, and owns rental property in Florida.

Key rules by jurisdiction:

| Jurisdiction | Safe Harbor? | Notes |

|---|---|---|

| Federal | Yes | Prior year method (100%/110%) |

| Virginia | Yes | Prior year method, similar to federal |

| California | Yes — but limited | Calculated only on California-sourced income |

| New York | Limited | Requires more precise current-year estimation |

| Florida | N/A | No state income tax |

Income allocation complexity:

- Consulting income: allocated to the state where work is performed

- Rental income: taxed by property location AND resident state

- Virginia (home state): taxes all income but credits taxes paid to other states

Multi-state tracking template — build a spreadsheet with these columns:

- Payment date (all quarterly deadlines)

- Jurisdiction (federal, each state)

- Amount (calculated payment per jurisdiction)

- Calculation method (Safe Harbor, estimated, etc.)

- Income source (which income triggers this obligation)

- Notes (special rules, credits, adjustments)

Questions to Ask a Tax Professional

Before hiring a tax advisor to help with estimated payments, ask these 3 questions:

| Question | Good Answer | Red Flag |

|---|---|---|

| ”How do you help clients avoid underpayment penalties while optimizing cash flow?” | Detailed explanation of Safe Harbor strategies with your specific numbers | Vague response about “paying enough" |

| "Can you walk me through the Safe Harbor calculation for my situation?” | Clear step-by-step walkthrough using your actual Line 24 and AGI | Can’t explain the concept or gives wrong percentages |

| ”How do you coordinate federal and state estimated tax planning?” | Discusses state-specific rules and multi-jurisdiction coordination | Only focuses on federal requirements |

Your 30-Day Implementation Plan

| Week | Actions |

|---|---|

| Week 1: Assessment | Locate last year’s Form 1040; identify Line 24 and Line 11; calculate your Safe Harbor target and quarterly payment amount |

| Week 2: Setup | Choose payment method (IRS Direct Pay, EFTPS, or bank bill pay); set calendar reminders for all 4 quarterly deadlines; open a dedicated tax savings account (recommended) |

| Week 3: First Payment | Make your first quarterly payment if one is currently due; confirm processing through your chosen method; update business cash flow projections |

| Week 4: Systematize | Document your Safe Harbor calculation for next year’s reference; set up automatic transfers to your tax savings account; schedule an annual Safe Harbor review for tax season |

Frequently Asked Questions

Q: What happens if I miss just one quarterly payment deadline?

Missing a deadline eliminates Safe Harbor protection for that quarter — but the situation is more nuanced than all-or-nothing. A few days late with documented reasonable cause (emergency, postal issue) may still qualify for protection with additional IRS paperwork, but it’s not guaranteed. Missing entirely means you cannot make up for it in the next quarter — each quarterly period stands alone. Making a larger Q3 payment does not retroactively fix a missed Q2. That said, paying late is always better than not paying at all — the IRS calculates penalties quarter by quarter.

Q: Can I pay more than my Safe Harbor requirement?

Yes — Safe Harbor sets the minimum for penalty protection, not a maximum. Any excess is credited toward your final tax bill. Many business owners intentionally pay 105% to 110% of their Safe Harbor target as a safety buffer.

Q: What if my income actually decreases this year?

Safe Harbor still protects you from penalties, but you will receive a larger refund at filing. Taxpayers with declining income sometimes prefer the 90% current-year method instead — but this requires accurate income forecasting, which reintroduces the estimation problem Safe Harbor is designed to solve.

Q: Do I need to file Form 1040-ES vouchers with my payments?

The 1040-ES vouchers are helpful for recordkeeping but are not required if you pay electronically through IRS Direct Pay, EFTPS, or bank bill pay. What matters is that the correct amount arrives by each deadline.

Q: Does Safe Harbor cover self-employment tax?

No. Safe Harbor applies only to income tax liability (Line 24). Self-employment tax (Schedule SE) requires its own separate estimated payments, and there is no Safe Harbor protection for SE tax underpayments. Calculate and add SE tax separately to your quarterly payments.

Q: Can I switch Safe Harbor methods mid-year?

No. Once you begin making payments under a chosen method, you are locked in for that tax year. You can select a different method the following year after reviewing your updated return.

Q: How does this work for married couples filing jointly?

Married couples calculate Safe Harbor based on their combined tax liability from the joint return. If spouses have separate businesses, they coordinate estimated payments to meet their combined Safe Harbor requirement.

Q: What about my first year in business with no prior return?

New business owners cannot use the prior-year Safe Harbor method — there is no baseline to reference. First-year owners must use the 90% current-year method, which requires estimating annual income and tax liability. Working with a tax professional during year 1 is strongly recommended to avoid penalties while establishing the baseline for future Safe Harbor calculations.

Q: I am an S-Corp owner. Does this work the same way?

S-Corp owners can use Safe Harbor for personal estimated payments, but the calculation is more complex. Your Safe Harbor requirement includes your allocable share of S-Corp income passing through to your personal return, plus all other personal income sources. The S-Corp itself may also have separate state-level estimated tax obligations requiring different planning.

Q: What if I have W-2 wages plus business income?

W-2 withholdings count toward your Safe Harbor requirement. You only need estimated payments for the remaining Safe Harbor amount after subtracting withholdings. For taxpayers with both W-2 income and significant self-employment or investment income, this coordination can substantially reduce the required quarterly cash outlay.

Key Takeaways

Safe Harbor transforms tax planning from reactive to proactive. Instead of scrambling each quarter to estimate current-year obligations, you make strategic payments based on historical, verifiable results.

The 5 principles that make it work:

- Use last year’s Line 24, not this year’s projections — eliminate guesswork entirely

- Apply 110% if your prior-year AGI exceeded $150,000 — no exceptions

- Treat quarterly deadlines as non-negotiable — 1 day late eliminates protection

- Research your state’s rules separately — federal Safe Harbor does not extend to states

- Review and recalculate annually — your Safe Harbor target changes every year based on your most recent return

Your next quarterly deadline is approaching. Calculate your number today, set up your payment system, and eliminate tax penalty anxiety permanently.

This article provides educational information about IRS Safe Harbor rules and is not personalized tax advice. Tax laws are complex and subject to change. Individual circumstances vary significantly. Before implementing any tax strategy, consult with a qualified tax professional who can review your complete financial picture, verify current requirements, and coordinate Safe Harbor with your state tax obligations and broader financial planning goals.