This article provides general educational information about inherited IRA rules and is not personalized tax, legal, or financial advice. Consult with qualified professionals for guidance specific to your situation.

When you inherit an IRA, you’re receiving more than just money. You’re stepping into a complex web of tax rules, distribution requirements, and strategic decisions that can dramatically impact how much you actually keep. The difference between making the right moves and the wrong ones? That could easily mean $100,000 or more over the next decade.

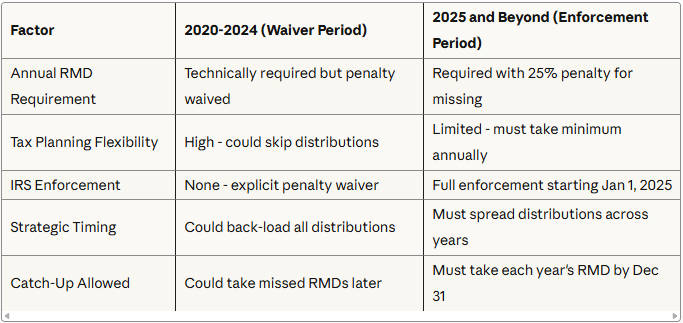

The 2025 enforcement change in one paragraph: The IRS finalized regulations in 2024 that fundamentally changed inherited IRA distributions starting January 1, 2025. If you inherited an IRA after 2019 from someone who had already started taking Required Minimum Distributions (RMDs), you must now take annual RMDs during the 10-year period — not just empty the account by year 10. The penalty waiver that protected beneficiaries from 2020 through 2024 has expired. Missing your 2025 RMD triggers a 25% penalty on the amount you should have withdrawn.

The 2025 Rule Change That Affects Inherited IRA Distributions

Starting January 1, 2025, the IRS began enforcing annual RMD requirements for inherited IRAs that were previously waived from 2020 through 2024. This is not a minor technical update.

What changed:

The IRS final regulations issued in July 2024 confirmed that if the original IRA owner had already started taking RMDs before death (had reached their Required Beginning Date), beneficiaries must:

- Take annual RMDs during years 1 through 9 of the 10-year period, AND

- Empty the account by December 31 of year 10

From 2020 through 2024, many beneficiaries and tax professionals interpreted the waiver guidance as meaning annual RMDs weren’t actually required. That interpretation is now definitively wrong.

The penalty for missing 2025 RMDs:

- 25% excise tax on the amount you should have withdrawn

- On a $50,000 required distribution: a $12,500 penalty

- You still owe income tax on the distribution when you eventually take it

- The IRS is not sending reminder notices

RBD = Required Beginning Date for RMDs, which is April 1 following the year the owner turns 73 — or 75 for those born in 1960 or later.

Real-World Impact: What This Means If You Inherited in 2020 Through 2024

Scenario: You inherited a $400,000 IRA in 2022 from your mother who was 78 when she passed (she had been taking RMDs). Under the waiver, you didn’t take RMDs in 2023 or 2024. You might have thought you could wait until 2032 (year 10) to take everything.

What you actually owe in 2025:

You must take your 2025 RMD by December 31, 2025 — or face a 25% penalty. Your RMD is calculated by dividing the December 31, 2024 account balance by your life expectancy factor from the IRS Single Life Expectancy Table.

- If you’re 50 years old, your life expectancy factor is approximately 36.2 years

- 2025 RMD: $400,000 / 36.2 = $11,050

- Miss the deadline: $2,763 penalty (25% of $11,050) plus income taxes when you eventually take it

For 2023 and 2024, the IRS waived penalties — you don’t owe back penalties for those years. But you must take RMDs for 2025, 2026, 2027, 2028, 2029, 2030, and 2031, then empty the account completely by December 31, 2032.

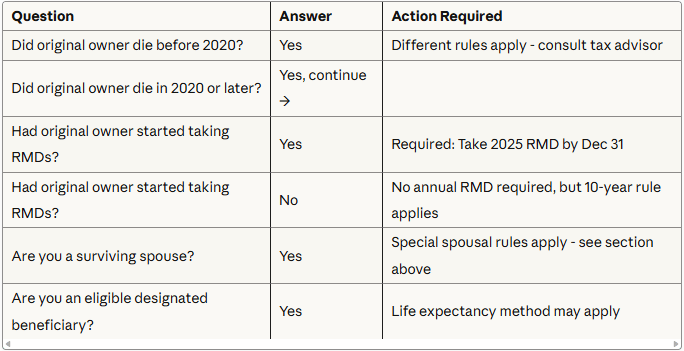

Understanding Who You Are in the Eyes of the IRS

The IRS categorizes beneficiaries into 3 distinct groups. Your group membership dictates your options, timelines, and tax consequences.

Spousal Beneficiaries: Maximum Flexibility

Spousal beneficiaries have options that no one else gets.

Option 1: Roll over into your own IRA

This is the most powerful option. The IRA becomes yours, you’re not subject to any immediate distribution requirements, and you won’t face RMDs until you reach age 73 (or age 75 if you were born in 1960 or later). The clock resets entirely.

Option 2: Remain as a beneficiary

This matters if you’re under age 59½ and might need access to money before traditional retirement age. When you remain as a beneficiary of an inherited spousal IRA, the 10% early withdrawal penalty is waived entirely. If you rolled the IRA into your own account, a $50,000 withdrawal would cost an extra $5,000 in penalties.

The tradeoff: remaining as a beneficiary requires you to take annual RMDs based on your life expectancy starting the year after your spouse’s death, rather than delaying until age 73.

Option 3: Keep in the deceased spouse’s name temporarily, then convert to your own IRA later when it’s more advantageous. This flexibility is exclusively available to spouses.

Real-world scenario: Maria, age 62

Maria inherits her husband’s $650,000 traditional IRA. Her husband was 67 when he passed. Maria has her own IRA worth $280,000 and is still working, earning $110,000 annually.

| Strategy | Details |

|---|---|

| Spousal rollover | Combined IRA of $930,000. No RMDs until age 73 (11 more years of growth). At 6% annually, the IRA could reach ~$1,760,000 by age 73. First RMD at 73: ~$66,000 |

| Remain as beneficiary | Must begin RMDs immediately. Life expectancy of 24.6 years. First RMD: ~$26,400. Over 10 years, she takes out approximately $330,000 |

The spousal rollover gives Maria control over timing — potentially letting her delay distributions until after retirement when her tax rate may be lower.

Non-Spouse Designated Beneficiaries: The 10-Year Rule

Named individual beneficiaries (children, siblings, friends, parents) face the 10-year distribution rule.

The core requirement: Empty the entire inherited IRA by December 31 of the 10th year following the year of the original owner’s death.

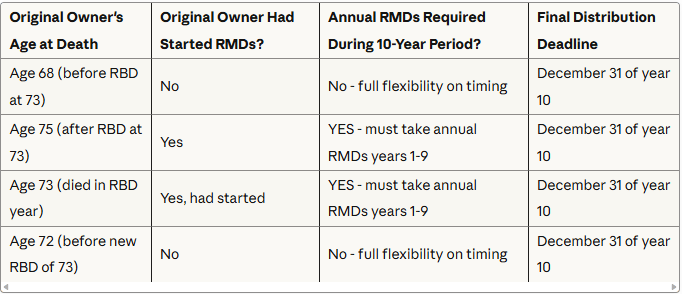

Annual RMD requirement (the 2025 change):

- If the original owner died before their Required Beginning Date: No annual RMDs required during the 10-year period. You can let the account grow and take everything in year 10.

- If the original owner died after their Required Beginning Date: Annual RMDs required during years 1 through 9, AND the account must be emptied by year 10.

Understanding the Annual RMD Requirement

Your Annual RMD Calculation Formula:

Account balance on December 31 of prior year / Your life expectancy factor (IRS Single Life Table)

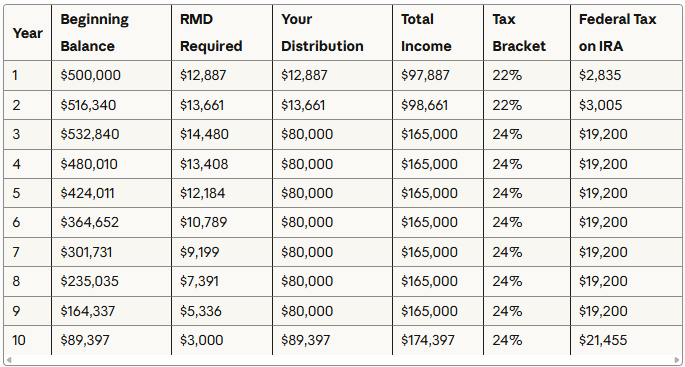

Example: You’re 45 years old, inherited a $500,000 IRA from a parent who was taking RMDs.

- Year 1 RMD: $500,000 / 38.8 = $12,887

- Each subsequent year, you divide the prior year-end balance by your remaining life expectancy (which decreases by 1 each year)

This requirement fundamentally changes your tax planning flexibility. Without it, you could strategically time all distributions to occur in low-income years. With it, you face a floor on distributions each year regardless of your tax situation. You gain flexibility only in choosing to take more than the minimum in any given year.

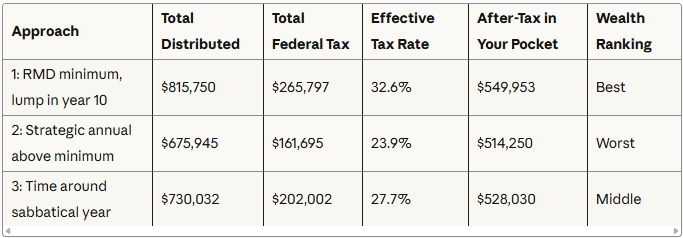

3 Distribution Approaches: A Case Study

Scenario for all 3 approaches:

- You inherit a $500,000 traditional IRA from a parent who was 76 and had already started RMDs

- You are 45 years old at the time of inheritance

- You earn $85,000 per year from your job (stays consistent except where noted)

- You are a single filer

- The inherited IRA grows at 6% annually

- Annual RMDs are required, AND the account must be empty by year 10

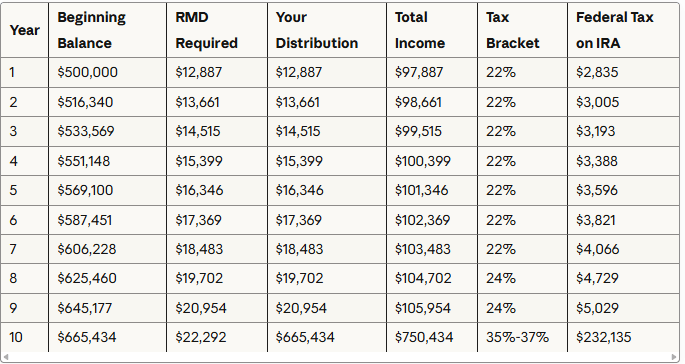

Approach 1: Take Only Required RMDs, Then Empty in Year 10

Takes the minimum required each year, lets the balance grow, then takes everything remaining in year 10.

Results:

| Metric | Amount |

|---|---|

| Total distributions | $815,750 |

| Federal taxes (years 1 through 9) | $33,662 |

| Federal taxes (year 10) | ~$232,135 |

| Total federal taxes | $265,797 |

| Effective tax rate on distributions | 32.6% |

| After-tax amount | $549,953 |

The counterintuitive result: Despite paying the most in taxes of all 3 approaches, Approach 1 puts the most money in your pocket. The extra $139,805 in distributions (generated by letting the account grow longer) more than compensates for the extra $104,102 in taxes. You end up with $35,703 more than Approach 2 and $21,923 more than Approach 3.

Key principle: Minimizing your tax rate and maximizing your after-tax wealth are not the same goal. Approach 1 is the least tax-efficient strategy but the most wealth-maximizing strategy.

Best fit: You don’t need distributions during years 1 through 9, can handle a large year 10 tax bill, and your primary goal is maximizing total after-tax wealth.

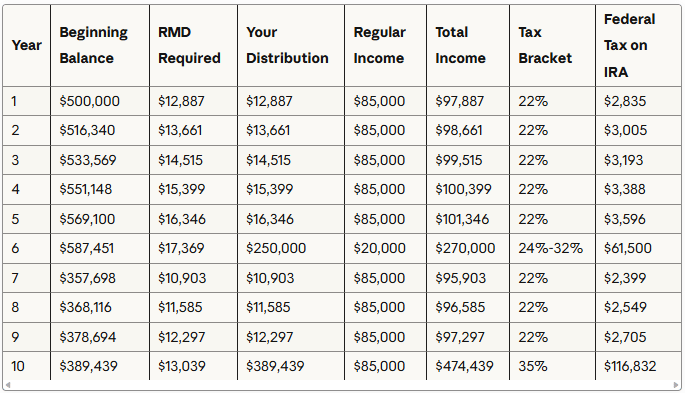

Approach 2: Strategic Annual Distributions Above the Minimum

Takes larger distributions each year ($80,000 annually starting in year 3) while still meeting RMD requirements.

Results:

| Metric | Amount |

|---|---|

| Total distributions | $675,945 |

| Total federal taxes | $161,695 |

| Effective tax rate on distributions | 23.9% |

| After-tax amount | $514,250 |

The tradeoff: Approach 2 is the most tax-efficient strategy (lowest effective rate, $104,102 less in taxes than Approach 1) — but it puts the least money in your pocket. By removing money from the tax-deferred account earlier, you sacrifice investment growth. The $104,102 saved in taxes is less valuable than the additional $139,805 in distributions Approach 1 generated.

Best fit: You need consistent cash flow during the 10-year period, want to avoid a single year of very high income (IRMAA surcharges, Medicare impacts, etc.), or value tax smoothing and certainty over maximum wealth accumulation.

Approach 3: Time Distributions Around Income Changes

You plan a sabbatical in year 6 when your income drops to $20,000. You take $250,000 during that low-income year and minimum RMDs in all other years.

Results:

| Metric | Amount |

|---|---|

| Total distributions | $730,032 |

| Total federal taxes | $202,002 |

| Effective tax rate on distributions | 27.7% |

| After-tax amount | $528,030 |

Where it lands: Middle ground. More wealth than Approach 2, less than Approach 1. The sabbatical year absorbs $250,000 at favorable rates (income of only $20,000), but a substantial year 10 balance still creates a tax spike.

Best fit: You have a predictable temporary income reduction window (sabbatical, career break, early retirement bridge, business startup, maternity/paternity leave) that you can plan around.

Comparison: All 3 Approaches

| Approach 1 | Approach 2 | Approach 3 | |

|---|---|---|---|

| Total distributions | $815,750 | $675,945 | $730,032 |

| Total federal taxes | $265,797 | $161,695 | $202,002 |

| Effective tax rate | 32.6% | 23.9% | 27.7% |

| After-tax wealth | $549,953 | $514,250 | $528,030 |

The surprising truth: The highest-tax approach delivers the most after-tax wealth. Tax efficiency and wealth maximization are not synonyms.

Eligible Designated Beneficiaries: The Exception to the 10-Year Rule

The SECURE Act created a special category that can still use a form of the old stretch IRA strategy — taking distributions over their life expectancy rather than facing the 10-year rule.

Who qualifies as an Eligible Designated Beneficiary:

- Surviving spouse

- Minor child of the deceased (until age 21 — then the 10-year rule kicks in)

- Disabled individuals (as defined by the IRS)

- Chronically ill individuals (as defined by the IRS)

- Any individual not more than 10 years younger than the deceased

That last category surprises people. If your 75-year-old brother names you as beneficiary and you’re 68, you qualify. But if you’re 66 when he dies at 80, you’re more than 10 years younger and face the 10-year rule.

Example: Thomas, age 71

Thomas inherits a $400,000 IRA from his 79-year-old sister. Because he’s within 10 years of her age, he qualifies as an Eligible Designated Beneficiary.

- Year 1 RMD: $400,000 / 17.0 (life expectancy at 71) = $23,529

- Year 2 RMD (after growth and first distribution): $392,000 / 16.0 = $24,500

This continues over Thomas’s lifetime — potentially 17+ years — compared to the 10-year rule that would require full distribution by year 10. Over 17 years, Thomas might withdraw $600,000 or more from the original $400,000 IRA.

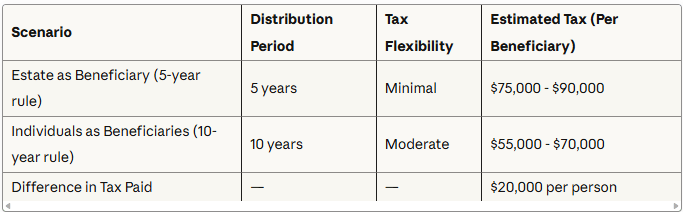

Non-Designated Beneficiaries: Estates, Charities, and Most Trusts

The least favorable category. Faces the most restrictive distribution rules.

The 5-year rule: If the original owner died before their Required Beginning Date, the entire IRA must be distributed by December 31 of the 5th year following the year of death — faster than the 10-year rule.

Why this matters for estate planning:

If your father’s $800,000 IRA names his estate as beneficiary (because he never updated the form after your mother passed), the estate faces the 5-year rule. Split equally among 3 siblings, each receives approximately $267,000 over 5 years.

If your father had named each of you individually as beneficiaries, you would each have had the 10-year rule — giving you far more flexibility to spread distributions across low-income years.

Multiply that across 3 beneficiaries, and the family pays $60,000 more in taxes simply because the beneficiary form wasn’t properly completed.

The Impact of the SECURE Acts: What Changed and Why It Matters

| Law | What it did |

|---|---|

| Pre-SECURE Act | ”Stretch IRA” — distributions over your entire life expectancy. A 30-year-old could take tiny distributions for 50+ years |

| SECURE Act (2019) | Eliminated the stretch IRA for most beneficiaries. 10-year rule became the new standard for non-spouse beneficiaries |

| SECURE Act 2.0 (2022) | Increased RMD age from 72 to 73 (effective 2023) and eventually to 75 (effective 2033) |

| 2024 IRS Final Regulations | Confirmed annual RMD requirement during the 10-year period when original owner had started RMDs. Effective January 1, 2025 |

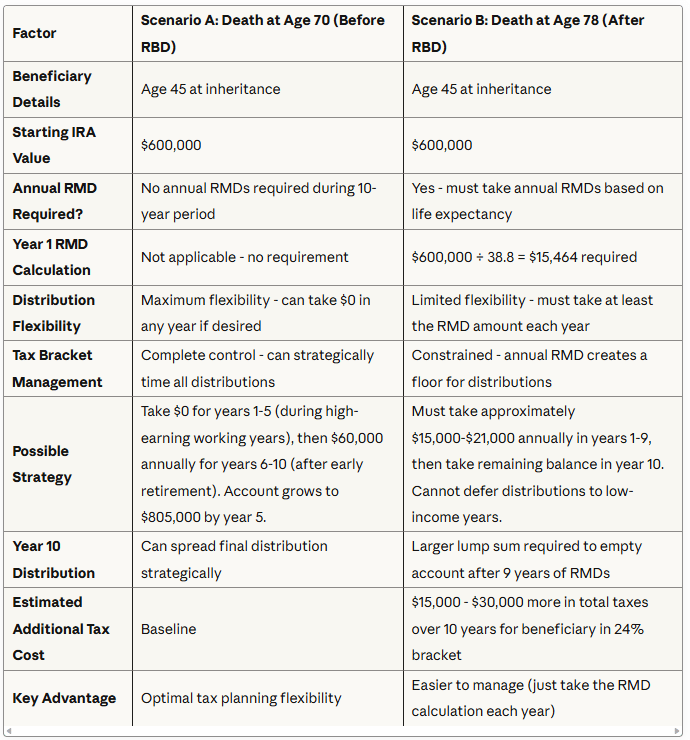

Why the Required Beginning Date matters — a side-by-side comparison:

Identical $600,000 inherited IRAs with one difference: the original owner’s age at death.

The original owner’s age at death determines whether you get complete distribution flexibility (death before RBD) or must take annual RMDs (death after RBD). This single factor can cost beneficiaries $15,000 to $30,000 in additional taxes over the 10-year period for a $600,000 inheritance.

How the 2025 One Big Beautiful Bill Act (OBBBA) Affects Your Planning

OBBBA, signed into law on July 4, 2025, didn’t change inherited IRA distribution rules — but it changed the tax landscape in which those distributions occur.

Key OBBBA Changes for Inherited IRA Beneficiaries

Standard deduction increases (permanent):

- Single filers: $15,750

- Married filing jointly: $31,500

- Indexed for inflation going forward

More of your income is protected from taxation before IRA distributions begin pushing you into higher brackets.

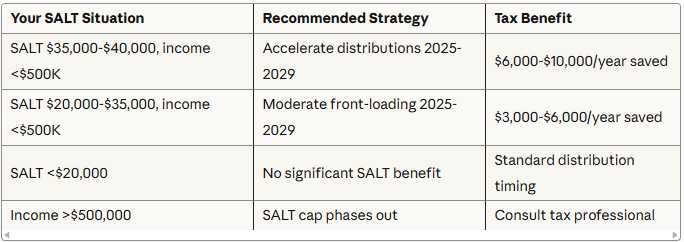

SALT deduction cap temporary increase (2025 through 2029):

- Old cap: $10,000

- New cap: $40,000 for taxpayers earning under $500,000

- Gradual 1% annual increase through 2029

- Taxpayers with MAGI over $500,000: cap reduced by 30% of income over that threshold

Estate and gift tax exemption increase (starting 2026):

- $15 million per person (from approximately $13.99 million in 2025)

- With portability for surviving spouses: $30 million per couple, indexed for inflation

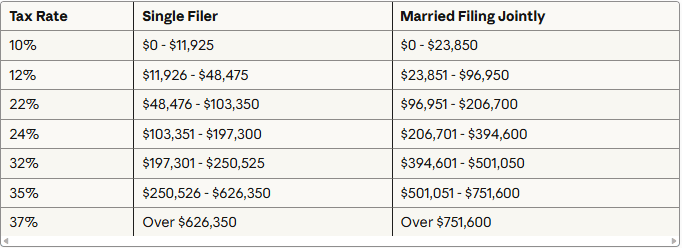

2025 Federal Income Tax Brackets (now permanent under OBBBA):

Plan your inherited IRA distributions with confidence — these brackets won’t sunset.

OBBBA Planning Opportunity: High-SALT-State Beneficiaries

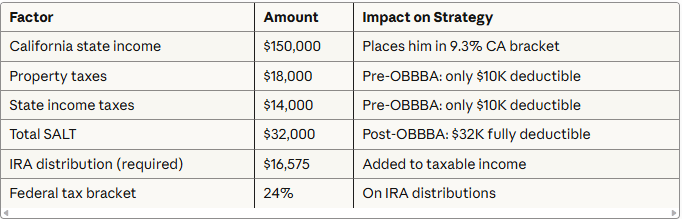

Scenario: David, California resident

David inherited a $600,000 IRA in 2024 from his father who had been taking RMDs. Annual RMDs apply.

| Before OBBBA (2024) | After OBBBA (2025) | |

|---|---|---|

| State and local taxes paid | $32,000 | $32,000 |

| SALT cap | $10,000 | $40,000 |

| SALT deduction claimed | $10,000 | $32,000 |

| Other itemized deductions | $32,000 | $32,000 |

| Total itemized deductions | $42,000 | $64,000 |

The OBBBA benefit:

- Additional deduction: $22,000

- Tax savings at 24% federal rate: $5,280 per year

- Over 10-year distribution period: $52,800 total savings

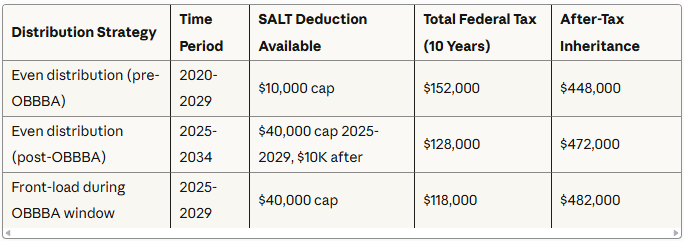

OBBBA Distribution Timing Strategy for High-SALT States

David saves $34,000 by front-loading distributions during the 2025 through 2029 window when the higher SALT cap is available — even though his marginal tax rate is higher with larger distributions. The SALT deduction more than compensates for bracket creep.

The critical deadline: The SALT deduction enhancement expires after 2029, reverting to $10,000. If your 10-year distribution period extends beyond 2029, strongly consider taking larger distributions during 2025 through 2029.

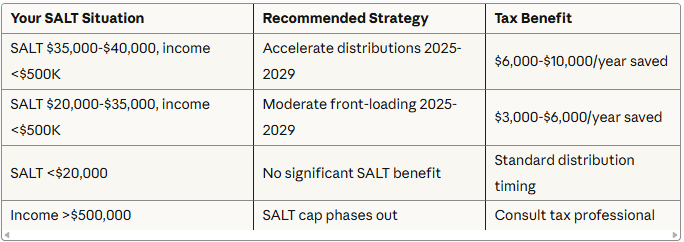

Recommended distribution strategies by SALT deduction level:

Senior Beneficiaries: Additional OBBBA Deduction (2025 Through 2028)

OBBBA added a temporary “bonus” deduction for taxpayers age 65 and older: $6,000 per person per year.

Phase-out thresholds:

| Filing Status | Phase-out begins | Phase-out rate |

|---|---|---|

| Single | $75,000 MAGI | 6% reduction per dollar over threshold |

| Married filing jointly | $150,000 MAGI | 6% reduction per dollar over threshold |

Example: Robert, age 67, inherited a $500,000 IRA. His 2025 income is $72,000. As a single filer age 65+, he qualifies for the full $6,000 deduction — saving approximately $1,440 in federal taxes annually (24% x $6,000) during 2025 through 2028.

If Robert’s income was $85,000: $85,000 - $75,000 = $10,000 over threshold. Reduction: $10,000 x 6% = $600. His bonus deduction: $6,000 - $600 = $5,400.

The Tax Reality: What “Inheriting” an IRA Actually Means

When someone tells you they inherited a $1,000,000 IRA, they didn’t really inherit $1,000,000. They inherited a tax liability wrapped around an asset. The actual after-tax value could be $750,000, $650,000, or even less, depending on their tax situation and distribution strategy.

Traditional IRAs contain pre-tax dollars. Every dollar you withdraw gets added to your taxable income for that year.

Understanding Your Effective Tax Rate on Distributions

Jennifer, single, $95,000 salary, inherits a $400,000 IRA

She decides to take $40,000 per year over 10 years. Total income: $135,000.

- Federal tax on $40,000 distribution: $9,547

- Effective rate on the distribution: 23.9%

If Jennifer instead took $80,000 in one year (total income: $175,000), her effective rate on the distribution: 23.8% — nearly identical, because both scenarios keep most of her income in the 24% bracket.

The real lesson: For someone at Jennifer’s income level, distribution size doesn’t dramatically change the tax rate as long as total income stays below $197,301 (the 32% bracket threshold). The tax planning opportunity comes from timing distributions in years when her income temporarily drops — not from splitting large amounts into smaller ones while income stays constant.

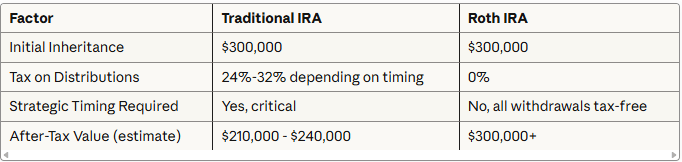

Inherited Roth IRAs: A Completely Different Tax Story

Roth IRAs contain after-tax dollars — qualified distributions are completely tax-free. You’re still subject to the same 10-year distribution rules, but there are no taxes on withdrawal.

Strategy difference: With a traditional inherited IRA, you carefully manage when you take distributions to avoid high-tax years. With an inherited Roth IRA, you let the entire account grow tax-free for 9 years, then withdraw everything in year 10, tax-free.

Example: A $300,000 inherited Roth IRA growing at 6% annually for 9 years reaches approximately $537,000 by year 10 — all withdrawn tax-free. You’ve received $237,000 in tax-free earnings over the period.

The Roth IRA inheritance is worth approximately $60,000 to $90,000 more after taxes — which is why estate planning often involves Roth conversions before death.

4 Common Mistakes That Cost Inherited IRA Beneficiaries

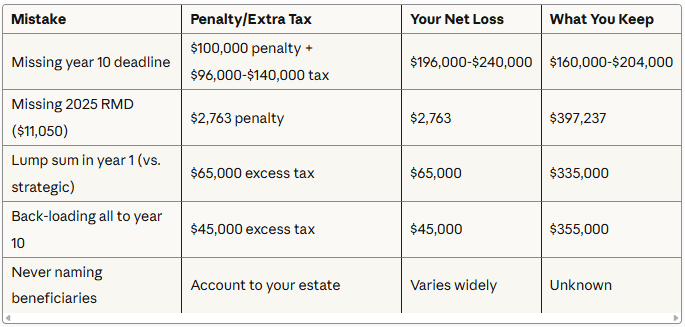

Mistake 1: Missing the December 31 Deadline in Year 10

The IRS doesn’t send reminders. Miss it and you face a 25% penalty on the remaining balance plus income taxes on the entire amount. On a $400,000 remaining balance: $100,000 penalty plus approximately $96,000 to $140,000 in income taxes (depending on bracket) — reducing a $400,000 inheritance to $160,000 to $204,000.

Mistake 2: Missing Annual RMDs When Required (2025 and Beyond)

Many beneficiaries who inherited from 2020 through 2024 don’t realize they now have annual RMD requirements. Penalty: 25% of the amount you should have withdrawn.

Mistake 3: Taking Everything in Year 1

A $500,000 distribution on top of a $100,000 salary pushes you into the 35% bracket — approximately $175,000 in federal taxes. Spreading it over 10 years at $50,000 annually might cost only $110,000 to $130,000 total.

Mistake 4: Failing to Update Your Own Beneficiary Designations

If you die during the 10-year period, the remaining inherited IRA balance passes according to your beneficiary designation. No named beneficiary means it passes to your estate — potentially triggering the 5-year rule and worse tax treatment for your heirs.

Your 2025 Action Plan

Phase 1: Immediate Actions (First 30 Days)

Step 1: Confirm your beneficiary category and distribution requirements

Contact the financial institution and obtain:

- Official date of death and original owner’s date of birth

- Confirmation that the original owner had or had not started taking RMDs

- Your beneficiary designation status

- Current account value

Step 2: Determine if you have a 2025 RMD due

Step 3: Calculate your 2025 RMD if required

RMD = Account balance on December 31, 2024 / Your life expectancy factor (IRS Single Life Table)

Example: You’re age 52, inherited $600,000 in 2022, account value was $620,000 on December 31, 2024.

- 2025 RMD = $620,000 / 34.4 (life expectancy for age 52) = $18,023

- Deadline: December 31, 2025

- Penalty for missing: $4,506 (25% of $18,023)

Phase 2: Strategic Planning (Days 30 Through 90)

Step 4: Create your 10-year tax distribution strategy

Map out your income projection for the next 10 years. Look for planned career changes, retirement timing, sabbaticals, or other income shifts.

Step 5: Consider OBBBA opportunities (2025 through 2029)

If you’re in a high-SALT state, consider front-loading distributions while the $40,000 SALT cap is available.

Step 6: Set up automated tracking and reminders

Critical dates to calendar:

| Date | What’s due |

|---|---|

| December 31 (each year) | Annual RMD deadline |

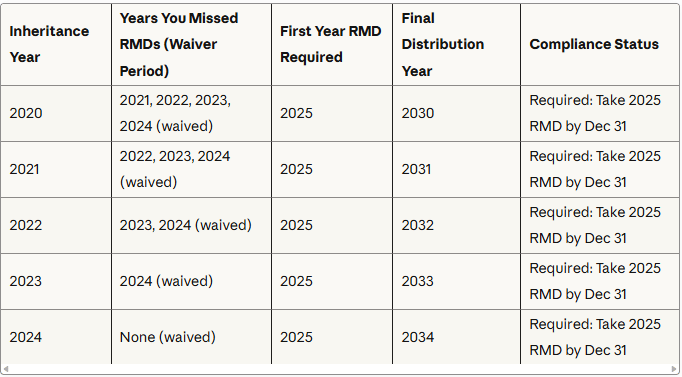

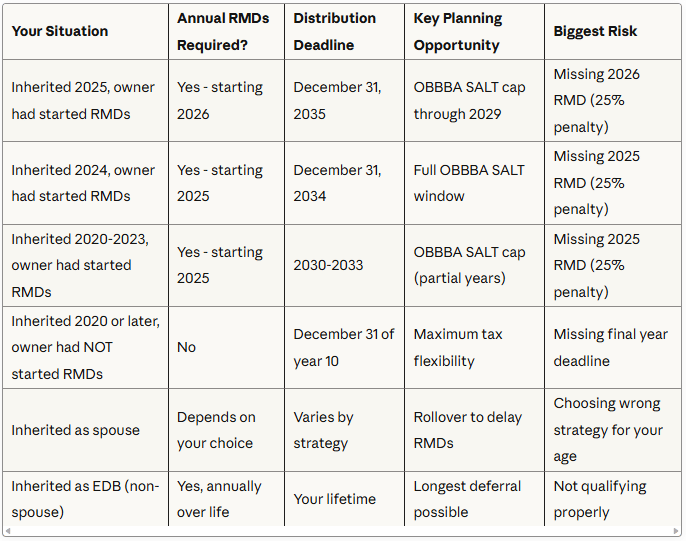

| December 31 of year 10 | Final distribution deadline (2030 for 2020 inheritances, 2031 for 2021, 2032 for 2022, 2033 for 2023, 2034 for 2024) |

| April 1 following the year you turn 73 | Your own RMDs begin (if applicable) |

| October 15 (each year) | Review and adjust strategy based on year-to-date income |

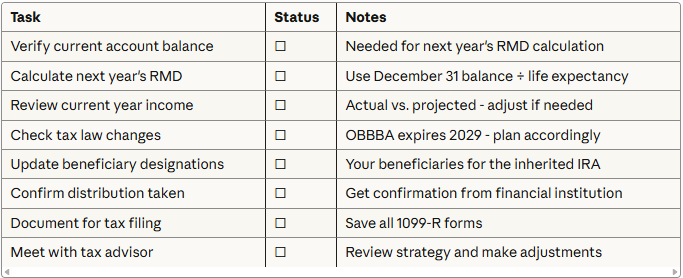

Phase 3: Annual Maintenance

Annual review checklist (complete by November 30 each year):

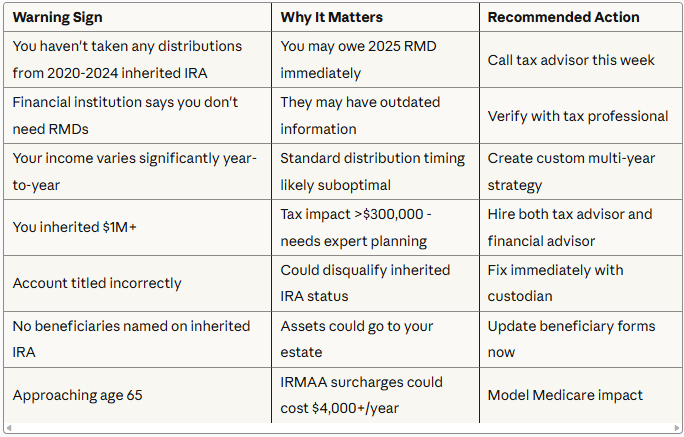

Critical 2025 Compliance Checklist (If You Inherited in 2020 Through 2024)

For inherited IRAs where the original owner HAD started RMDs:

For inherited IRAs where the original owner had NOT started RMDs:

You have maximum flexibility — no annual RMDs required during the 10-year period. But you must still empty the account by December 31 of the 10th year following death.

When Professional Help Is Worth the Cost

| Inherited IRA Value | Professional Fees | Potential Tax Savings | ROI |

|---|---|---|---|

| Over $250,000 | $500 to $2,000 (one-time consultation) | $15,000 to $75,000 over 10 years | 750% to 3,750% |

| Over $1,000,000 | $2,500 to $5,000 annually | $100,000 to $300,000 over 10 years | 400% to 1,200% |

Consider professional help immediately if:

- You’re in a high-SALT state with income near $500,000

- You’re approaching Medicare age and concerned about IRMAA surcharges

- You inherited multiple IRAs from different people

- You’re a trust beneficiary

- The original owner had both traditional and Roth IRAs

- You’re planning major life changes (retirement, business sale, etc.)

Quick Reference: Your Inherited IRA at a Glance

The 3 Rules That Matter Most

Rule 1: Know your deadline

- Annual RMDs required: December 31 every year

- Final distribution: December 31 of year 10

- Penalty for missing: 25% of required amount

Rule 2: Plan for taxes

- Every dollar is taxable income (except Roth IRAs)

- State taxes can add 0% to 13.3% on top of federal

- Strategic timing can save $50,000 to $150,000 on a $500,000 inheritance

Rule 3: Use the 2025 through 2029 OBBBA window

- Higher SALT deduction ($40,000 vs. $10,000) expires after 2029

- If you’re in a high-tax state, front-load distributions during this window

- Potential savings: $30,000 to $70,000 for high-SALT taxpayers

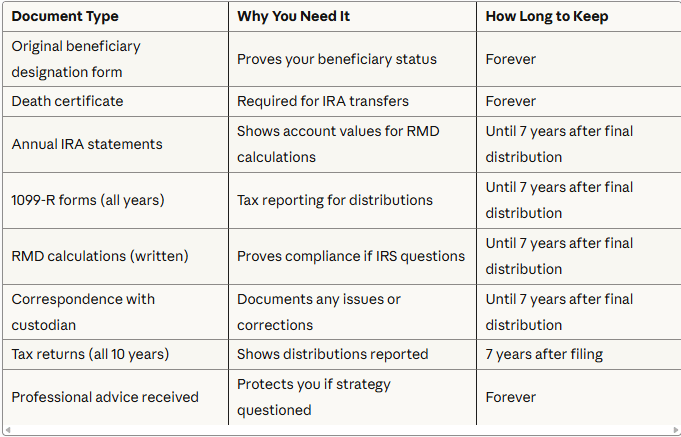

Document Retention Checklist

Keep these documents for the entire 10-year distribution period, plus 7 years after:

Further Reading

IRS resources:

- Publication 590-B: Distributions from Individual Retirement Arrangements

- IRS Retirement Plans: Beneficiary Rules and Life Expectancy Tables

Tax law changes:

- SECURE Act 2.0 provisions

- State tax impacts: Search “[Your state] department of revenue inherited IRA”

This article provides general educational information, not personalized tax, legal, or financial advice. Tax laws change frequently. Consult qualified professionals before making decisions about an inherited IRA. Individual circumstances vary, and strategies discussed may not be appropriate for your situation. The 2025 tax brackets and OBBBA provisions referenced reflect law as of the publication date.