You contributed $7,000 to your Roth IRA in January, feeling good about your retirement discipline. Then December arrives, and you realize your income — bonuses, stock options, a strong business year — pushed you over the Roth IRA income limit. Your stomach drops.

Take a breath. This situation is common among high earners with variable income, and there is a completely legal fix that costs you nothing in penalties.

Roth IRA Income Limits and Contribution Caps

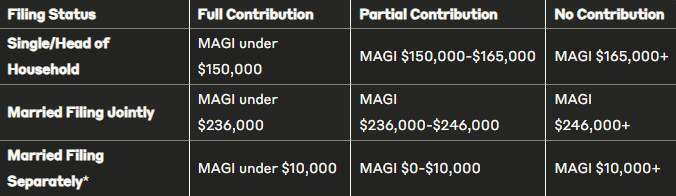

The IRS sets income thresholds that determine Roth IRA eligibility. These are based on Modified Adjusted Gross Income (MAGI) — not your gross salary.

Annual Contribution Limits by Age

| Age | Annual Roth IRA Limit |

|---|---|

| Under 50 | $7,000 |

| 50 and older (catch-up eligible) | $8,000 |

Income Phase-Out Ranges by Filing Status

Married filing separately: If you lived with your spouse at any point during the year, the phase-out begins at $0 MAGI and eliminates eligibility at $10,000.

What Is MAGI?

MAGI is not the same as your W-2 salary or even your standard AGI. It adds certain deductions back to your AGI, including:

- Student loan interest deduction

- Foreign earned income exclusion

- Traditional IRA deduction

- Self-employment tax deduction

For most W-2 employees, MAGI and AGI are identical or very close. For self-employed taxpayers and those with foreign income, the difference can be significant.

The Penalty for Doing Nothing

An excess Roth IRA contribution triggers a 6% excise tax per year for every year the excess remains in the account. This is not a one-time penalty — it recurs annually until the problem is corrected.

| Excess Amount | Annual Penalty | 3-Year Total if Unaddressed |

|---|---|---|

| $1,000 | $60/year | $180 |

| $3,000 | $180/year | $540 |

| $7,000 | $420/year | $1,260 |

The clock starts ticking from the tax year of the excess contribution. Acting promptly eliminates all future accruals.

The Solution: Recharacterization + Backdoor Roth Conversion

The fix is a 2-step process that transforms an ineligible Roth contribution into a perfectly legal one.

| Step | What Happens | Tax Impact |

|---|---|---|

| Step 1: Recharacterization | Move the excess Roth contribution (plus earnings) into a traditional IRA | No tax event — treated as if the original contribution was made to the traditional IRA |

| Step 2: Backdoor Roth Conversion | Convert the traditional IRA funds back to your Roth IRA | Tax owed only on earnings generated while funds were in the traditional IRA |

Think of it as rerouting around the income restriction. Conversions from traditional IRA to Roth IRA have no income limits — only direct Roth contributions do.

Step-by-Step Implementation

Step 1: Open a Traditional IRA (If Needed)

If you do not already have one, open a traditional IRA with the same custodian that holds your Roth IRA. Using the same institution avoids inter-custodian transfer delays.

Step 2: Request the Recharacterization

Contact your IRA custodian and request a recharacterization of your Roth contribution due to income limits.

What to tell them:

- “I need to recharacterize my [year] Roth IRA contribution to a traditional IRA due to exceeding income limits”

- Specify the exact contribution amount

- Request that all attributable earnings (or losses) also be transferred

Critical: You must move both the original contribution and any earnings or losses it generated. The custodian calculates the earnings amount using the IRS Net Income Attributable (NIA) formula — you do not need to calculate this yourself.

Step 3: Wait for Completion

Recharacterizations typically take 3 to 7 business days. Do not proceed to the conversion until the funds are fully settled in the traditional IRA.

Step 4: Execute the Backdoor Roth Conversion

Once the funds sit in the traditional IRA, convert them immediately to your Roth IRA. Because conversions have no income limits, this step is available to anyone regardless of income.

Tax on conversion: You owe ordinary income tax only on the earnings that accrued while the money was in the traditional IRA — not on the original contribution, which was already made with after-tax dollars.

Step 5: Understand the Pro Rata Rule

This is where most people make expensive mistakes. The pro rata rule determines how much of your conversion is taxable based on the ratio of pre-tax to after-tax money across all your IRA accounts.

The formula:

Taxable Portion = (Pre-tax IRA Balance / Total IRA Balance) × Conversion AmountWhat counts as “IRA balance” for pro rata purposes:

| Counts | Does Not Count |

|---|---|

| Traditional IRAs | Roth IRAs |

| Rollover IRAs | 401(k), 403(b), 457(b) plans |

| SEP IRAs | |

| SIMPLE IRAs (after 2-year seasoning period) |

The pro rata rule looks at your December 31st IRA balance for the year of conversion — not the balance at the time you execute the conversion.

Worked Example 1: Sarah’s $50,000 Rollover Problem

Sarah’s situation:

| Item | Amount |

|---|---|

| Filing status | Single |

| 2025 income | $170,000 (above $165,000 limit) |

| Excess Roth contribution | $7,000 |

| Earnings on excess contribution | $200 |

| Existing rollover IRA (old 401k) | $50,000 |

Sarah recharacterizes: $7,200 ($7,000 + $200 earnings) moves to her traditional IRA.

Sarah’s pro rata problem:

| Item | Amount |

|---|---|

| Total IRA balance (Dec 31) | $57,200 ($50,000 + $7,200) |

| Pre-tax portion (rollover IRA) | $50,000 |

| Taxable conversion amount | ($50,000 / $57,200) × $7,200 = $6,294 |

Sarah would owe taxes on $6,294 — nearly the entire conversion amount. Not the intended outcome.

Sarah’s smart fix: Before converting, she rolls her $50,000 rollover IRA into her current employer’s 401(k). Now her only IRA balance is the $7,200 from the recharacterization.

New calculation after 401(k) rollover:

| Item | Amount |

|---|---|

| Total IRA balance (Dec 31) | $7,200 |

| Pre-tax portion | $0 |

| Taxable conversion amount | $200 (earnings only) |

By rolling her old 401(k) money out of IRA territory, Sarah reduced her tax exposure from $6,294 to $200.

Worked Example 2: Michael’s Clean Conversion

Michael’s situation:

| Item | Amount |

|---|---|

| Filing status | Married filing jointly |

| 2025 combined income | $250,000 (above $246,000 limit) |

| Age | 45 |

| Excess Roth contribution | $7,000 |

| Earnings on contribution | $300 |

| Other IRA balances | None |

Michael’s process:

| Step | Action | Amount |

|---|---|---|

| Recharacterization | Moves $7,300 to traditional IRA | $7,000 + $300 earnings |

| Conversion | Converts $7,300 back to Roth IRA | Full amount |

| Taxable amount | Only the earnings | $300 |

| Tax owed (24% bracket) | $300 × 24% | $72 |

Compared to doing nothing:

| Option | Cost |

|---|---|

| Recharacterization + conversion | $72 (one-time tax on earnings) |

| 6% annual penalty on $7,000 | $420/year, every year until fixed |

Michael saves $420 per year by fixing this correctly.

Form 8606: Required Paperwork

Form 8606 is how you report nondeductible IRA contributions and Roth conversions to the IRS. It must be filed with your tax return for the year of the conversion.

| Form Section | What It Reports |

|---|---|

| Part I | Nondeductible traditional IRA contributions |

| Part II | Roth IRA conversions |

| Part III | Roth IRA distributions (if applicable) |

If you skip Form 8606: The IRS assumes your entire conversion is taxable — meaning you pay income tax on dollars that were already taxed. This mistake can cost thousands in unnecessary taxes.

Key Deadlines

| Deadline | What It Covers |

|---|---|

| December 31 of the tax year | Last day to complete the conversion and avoid pro rata complications from year-end IRA balances. Roll old IRAs into a 401(k) before this date if needed. |

| April 15 of the following year | Tax filing deadline AND last day to recharacterize a prior-year Roth contribution |

| October 15 of the following year | Extended filing deadline (recharacterization deadline does NOT extend — April 15 is the hard cutoff) |

Best practice: Complete both the recharacterization and the conversion well before December 31 to ensure everything settles properly and December 31 balances are clean.

4 Common Mistakes

Mistake 1: Not moving earnings with the contribution

Recharacterizing only the contribution amount and leaving earnings in the Roth IRA. Those earnings become their own excess contribution, subject to their own 6% annual penalty.

Mistake 2: Ignoring other IRA balances

Forgetting about rollover IRAs, SEP IRAs, or SIMPLE IRAs when calculating the pro rata ratio. The result: unnecessary taxes on the conversion.

Mistake 3: Missing the April 15 deadline

The recharacterization deadline is April 15 of the year following the contribution — it does not extend with your tax return. Miss it and the 6% penalty becomes permanent for that year.

Mistake 4: Skipping Form 8606

Not filing the required form. The IRS defaults to treating the entire conversion as taxable income. Filing Form 8606 is the only mechanism to establish the after-tax basis that protects you.

Is This Strategy Right for You?

| Situation | Recharacterization + Backdoor Conversion |

|---|---|

| Accidentally contributed over income limits | Strong fit |

| No other traditional IRA balances | Strong fit — pro rata problem is minimal |

| Can roll existing IRAs into a 401(k) | Strong fit — clears the pro rata issue |

| Large traditional IRA balances with no 401(k) to absorb them | Weak fit — pro rata will make conversion mostly taxable |

| Income only slightly over the limit | Consider a simple withdrawal instead — may be simpler |

| Multiple years of excess contributions to unwind | Consult a tax professional — sequencing matters |

Advanced Option: The Mega Backdoor Roth

If you have access to a 401(k) that allows after-tax contributions and in-service withdrawals, the mega backdoor Roth strategy enables annual contributions up to $70,000+ into Roth accounts — far beyond the standard $7,000 limit. This strategy involves after-tax 401(k) contributions, in-plan conversions or in-service rollovers, and careful coordination with HR and plan documents. Not all 401(k) plans offer these features.

When to Bring In a Professional

The recharacterization strategy is conceptually straightforward but has enough moving parts to warrant professional guidance in several situations:

| Situation | Why Professional Help Matters |

|---|---|

| Multiple IRA accounts across different custodians | Complex pro rata mapping; consolidation opportunities |

| Large dollar amounts involved | A miscalculation costs more than the advisor’s fee |

| SEP IRA or SIMPLE IRA from a business | These interact with pro rata in ways that create unexpected tax consequences |

| Multiple years of excess contributions | Unwinding several years requires careful sequencing |

| Discomfort with Form 8606 | Small errors on this form can have large downstream tax consequences |

A qualified tax professional can also represent you if the IRS has questions about the transaction. The typical consultation cost for this type of issue pays for itself by avoiding a single year of unnecessary penalties.

The Bottom Line

An excess Roth IRA contribution does not have to result in penalties. The recharacterization plus backdoor conversion strategy is a legal, well-established pathway that leaves you exactly where you intended to be — with after-tax dollars growing in a Roth IRA — without paying a cent in penalties.

The key variables:

- Act before April 15 of the following year

- Resolve the pro rata problem by rolling pre-tax IRAs into a 401(k) before December 31 if needed

- File Form 8606 with your return — skipping it is expensive

- Move earnings along with the contribution when recharacterizing

The goal is not just to fix the mistake — it is to set up a system where you can continue building tax-free retirement wealth regardless of how high your income climbs.

This article is for educational purposes only and should not be construed as personalized tax, legal, or financial advice. Tax laws are complex and subject to change. Income limits, contribution amounts, and tax rates referenced here are based on current law and are subject to adjustment by the IRS or Congress. Individual circumstances vary significantly — consult a qualified tax professional, CPA, or enrolled agent before implementing any strategy discussed here, particularly if you have complex retirement account arrangements, own a business, or have multiple years of excess contributions to address.