Understanding Required Minimum Distributions (RMDs): A Comprehensive Guide for Retirees

Navigate Your Retirement with Confidence: Learn the Essentials of RMDs, Their Calculations, and Avoiding Penalties

Prashanth Srikanthan

6/15/20245 min read

Planning for retirement is a multifaceted process that involves not just saving and investing but also understanding the rules around withdrawals. One key concept that retirees must grasp is the Required Minimum Distribution (RMD). This blog post will explain what RMDs are, why they exist, how they are calculated, and what happens if you fail to take them.

What Are Required Minimum Distributions (RMDs)?

RMDs are mandatory withdrawals that must be taken annually from certain retirement accounts once you reach a specific age. The purpose of RMDs is to ensure that individuals eventually pay taxes on their tax-deferred retirement savings. These distributions apply to traditional IRAs, SEP IRAs, SIMPLE IRAs, and employer-sponsored retirement plans such as 401(k)s, 403(b)s, and 457(b)s.

Why Do RMDs Exist?

RMDs exist primarily to ensure that retirement funds, which have enjoyed tax-deferred growth, are eventually subject to income tax. The IRS allows individuals to defer taxes on the income and growth of their retirement savings during their working years, but it requires these funds to be taxed at some point. RMDs serve this purpose by mandating withdrawals starting at a certain age, thus bringing the funds into taxable income.

When Do RMDs Start?

As of the SECURE Act passed in December 2019, the age at which RMDs must begin was increased from 70½ to 72. This means that if you turned 72 on or after January 1, 2020, you must start taking RMDs by April 1 of the year following the year you turn 72. For subsequent years, the RMD must be taken by December 31.

How Are RMDs Calculated?

The calculation of RMDs involves several steps:

Determine the Account Balance: Identify the balance of your retirement account as of December 31 of the previous year.

Find the Distribution Period: Use the IRS Uniform Lifetime Table to find the distribution period (or life expectancy factor) that corresponds to your age. The table provides a divisor based on your age.

Calculate the RMD: Divide the account balance by the distribution period to determine your RMD for the year.

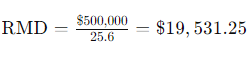

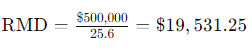

For example, if you are 72 years old with a retirement account balance of $500,000, and the distribution period for your age is 25.6, your RMD would be calculated as follows:

Use this RMD Calculator to calculate your RMD.

Special Considerations

Multiple Accounts: If you have multiple retirement accounts, you must calculate the RMD for each one separately. However, you can choose to withdraw the total RMD amount from one or more accounts.

Inherited Accounts: If you inherit a retirement account, different RMD rules apply depending on your relationship to the deceased and the type of account.

Tax Implications of RMDs

Understanding the tax implications of RMDs is crucial for effective retirement planning. Here are some key points:

Taxable Income: RMDs are generally considered taxable income. This means that the amount you withdraw is added to your income for the year and taxed at your current income tax rate. For example, if your RMD for the year is $20,000, this amount will be included in your taxable income.

Tax Bracket Impact: Large RMDs can push you into a higher tax bracket, increasing your overall tax liability. It's important to plan your withdrawals strategically to minimize the tax impact.

State Taxes: In addition to federal taxes, you may also owe state income taxes on your RMDs, depending on where you live.

Social Security Benefits: Increased income from RMDs can affect the taxation of your Social Security benefits. Up to 85% of your Social Security benefits can be taxed if your income exceeds certain thresholds.

Medicare Premiums: Higher income from RMDs can also impact your Medicare premiums. If your income exceeds certain levels, you may have to pay higher premiums for Medicare Part B and Part D.

Real-World Examples

Example 1: John’s RMD and Tax Implications

John is 72 years old and has a traditional IRA with a balance of $600,000. According to the IRS Uniform Lifetime Table, the distribution period for his age is 25.6. His RMD for the year would be:

RMD = $600,000 / 25.6 = $23,437.50

John's annual income from other sources, including Social Security, is $40,000. Adding his RMD of $23,437.50, his total taxable income for the year becomes $63,437.50.

If John’s tax bracket for the combined income is 24%, he would owe:

$23,437.50 × 0.24 = $5,625 in federal taxes on the RMD.

Example 2: Mary's RMD Impact on Medicare Premiums

Mary is 75 years old and has a traditional 401(k) with a balance of $800,000. Using the distribution period of 22.9 for her age, her RMD is:

RMD=$800,000 / 22.9 = $34,934.50

Mary’s other income sources, including a pension and Social Security, amount to $50,000 per year. Her total income including the RMD is:

$50,000 + $34,934.50 = $84,934.50

Because Mary's income exceeds the threshold for higher Medicare premiums, she must pay increased premiums for Medicare Part B and Part D.

Example 3: Roth Conversion Strategy

David, who is 65 years old, decides to convert a portion of his traditional IRA to a Roth IRA before reaching RMD age. He converts $100,000, paying taxes on the converted amount now at his current tax rate. This reduces the balance in his traditional IRA, thereby lowering his future RMDs and potentially keeping him in a lower tax bracket when he starts taking RMDs.

What If You Fail to Take an RMD?

Failing to take the full RMD amount by the deadline can result in a hefty penalty. The IRS imposes a 50% excise tax on the amount not withdrawn. For example, if your RMD is $20,000 and you only withdraw $10,000, you could be penalized $5,000 (50% of the $10,000 shortfall).

Strategies to Manage RMDs

There are several strategies you can employ to manage RMDs effectively:

Qualified Charitable Distributions (QCDs): Individuals over age 70½ can direct up to $100,000 annually to a charity directly from their IRA, satisfying the RMD requirement without adding to taxable income.

Roth Conversions: Converting a portion of traditional IRA funds to a Roth IRA before reaching RMD age can reduce the amount subject to RMDs, as Roth IRAs do not have RMDs during the owner's lifetime.

Withdrawal Planning: Developing a strategic withdrawal plan that considers tax brackets and future income needs can help minimize the tax impact of RMDs.

Conclusion

Understanding RMDs is crucial for effective retirement planning. These mandatory withdrawals ensure that tax-deferred retirement savings eventually become taxable, providing the government with revenue. By knowing when RMDs start, how they are calculated, and the penalties for non-compliance, you can better manage your retirement funds and minimize tax liabilities. Employing strategies like QCDs and Roth conversions can also help optimize your retirement income. Always consider consulting with a financial advisor to tailor an RMD strategy that fits your unique financial situation.

To get started on creating a personalized financial plan, book a clarity call with one of our experienced advisors. Our team is here to guide you every step of the way, ensuring you have the knowledge and tools to build a secure and prosperous retirement. Schedule your clarity call today and take the first step towards a financially confident future.